Recent tax changes mean more taxpayers may now qualify as a “cash basis person” under New Zealand’s financial arrangement rules.

From the 2025–26 income year, the thresholds for using the cash basis have increased. This is a helpful change for many individuals, smaller investors, and taxpayers with term deposits, bonds, foreign currency accounts, or other financial arrangements.

In simple terms, being a cash basis person usually means you do not have to spread income and expenses from financial arrangements over the life of the arrangement. Instead, you generally return income and claim expenses on a cash basis during the term of the arrangement. A wash-up calculation, known as a base price adjustment, is usually required when the arrangement ends.

What were the previous thresholds?

Before the changes, taxpayers generally needed to satisfy the relevant cash basis person tests, which included:

• income and expenditure from financial arrangements of $100,000 or less; or

• total financial arrangements of $1,000,000 or less; and

• a separate deferral threshold

That deferral threshold often added complexity, as it required taxpayers to compare the result under an accrual basis with the result under a cash basis.

What has changed?

From the 2025–26 income year, the main thresholds have doubled:

• the income and expenditure threshold has increased to $200,000; and

• the total financial arrangements threshold has increased to $2,000,000

• the deferral threshold has also been removed from 1st April 2026, making the rules easier to apply

This means more taxpayers may now be able to return income from financial arrangements on a cash basis, rather than needing to calculate income on an accrual basis each year.

What is a financial arrangement?

A financial arrangement is broadly defined under the Income Tax Act. It generally covers arrangements involving money, debt, or the lending of money where interest, finance charges, or other returns are involved.

Common examples include:

• bank term deposits;

• bonds and debentures;

• loans and mortgages;

• foreign currency accounts; and

• some deferred payment arrangements

Some arrangements are specifically excluded from the financial arrangement rules, so it is important to check the treatment of each arrangement rather than assuming all investments are treated the same way.

Why does this matter?

The financial arrangement rules can sometimes require income to be calculated on an accrual basis. This can mean tax is payable on income that has been earned but not yet paid in cash.

For some taxpayers, that can create a cash flow issue – particularly where interest is only paid at the end of an investment term.

The higher thresholds should make life easier for more individuals and smaller investors by reducing the need for detailed accrual calculations. It may also help reduce compliance costs.

This change may be especially relevant for taxpayers with:

• term deposits or fixed-interest investments;

• bonds;

• foreign currency accounts or deposits;

• loans or mortgages; or

• managed investment portfolios

Example

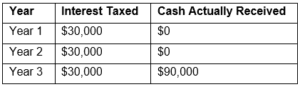

Say you invest $500,000 into a three-year term investment paying 6% simple interest each year, with all interest paid at the end of the three-year term.

Under the accrual basis

Part of the interest income may be taxable each year as it is earned, even though no cash has yet been paid to you.

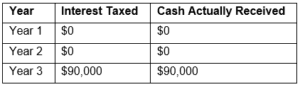

Under the cash basis

If you qualify as a cash basis person, you generally return the income when it is received.

This can make cash flow easier to manage, especially where the investment does not pay interest until maturity.

What should you do?

If you were previously above the old thresholds but now fall within the new limits, you may be able to change to the cash basis method.

The approach will depend on your specific investments and tax position. Changing from a cash basis to an accrual basis (or vice versa) is not just a simple flip of the switch. Specific transitional adjustments are required to ensure that no income is omitted, and no expenditure is claimed twice. Under the financial arrangement rules, a wash-up calculation – effectively a Base Price Adjustment (BPA) – is required to ensure that the overall tax outcome is correct.

For clients with managed portfolios, the annual tax reports provided by portfolio providers may already include accrual-based calculations. In those cases, the practical benefit of changing to the cash basis may need to be weighed against any compliance cost or adjustment required. For our clients, we will review your portfolio’s on a case-by-case basis to determine the best outcome for you.

If you have any queries about this change and how it may apply to you, do not hesitate to contact our team.